2022 has been a challenging year. At 9 months, the current bear market is the longest we’ve seen since the financial crisis in 2008. The average length of a bear market since 1929 is 14 1/2 months, but the length of bear markets comes with a lot of variability. The longest bear market on record was 36 months, and the shortest was in 2020 at just 1 month. We are defining a bear market as the S&P 500 being down by more than 20%. History has proven over and over that predicting capitulation in the market itself is no easy task. Here is a look at the drawdowns since March 16, 2009, the lowest point of the market after the 2007-2009 bear market.

While the S&P is about 24% down from its high, the Nasdaq is about 34% down and the bond market has been historically bad. Many stocks outside of the major indexes are down more than 90%, stocks of companies that many consider quality investments. The bullet-proof 60/40 portfolio that has done fantastic on a risk-adjusted basis over the years is down about 21% year-to-date. Only 1931 was worse at 27%.

Clearly, the S&P 500 doesn’t accurately represent what a difficult year it has been for investors.

The bond market has left conservative investors reeling. Traditionally used for income, bonds have been used mostly as a portfolio hedge over the past 15 years while interest rates have been low. The rise in target rates by central banks around the world isn’t necessarily a surprise, but the speed of those rate increases in response to inflation has been problematic. The charts below represent the US and global bond markets over the past 10 years.

Why not jump out of bonds now? It is reasonable to expect that as inflation starts to ease and stronger recessionary signals penetrate markets, central banks will start to reverse course. If they do, bond values will go back up. It’s also important to understand that there is a degree of risk premium built into bond prices (expectations of future rate increases). Trying to time the bond market will be as difficult as trying to time the stock market. Bond values may be down, but yields are higher and more attractive going forward. This is positive for conservative investors long-term.

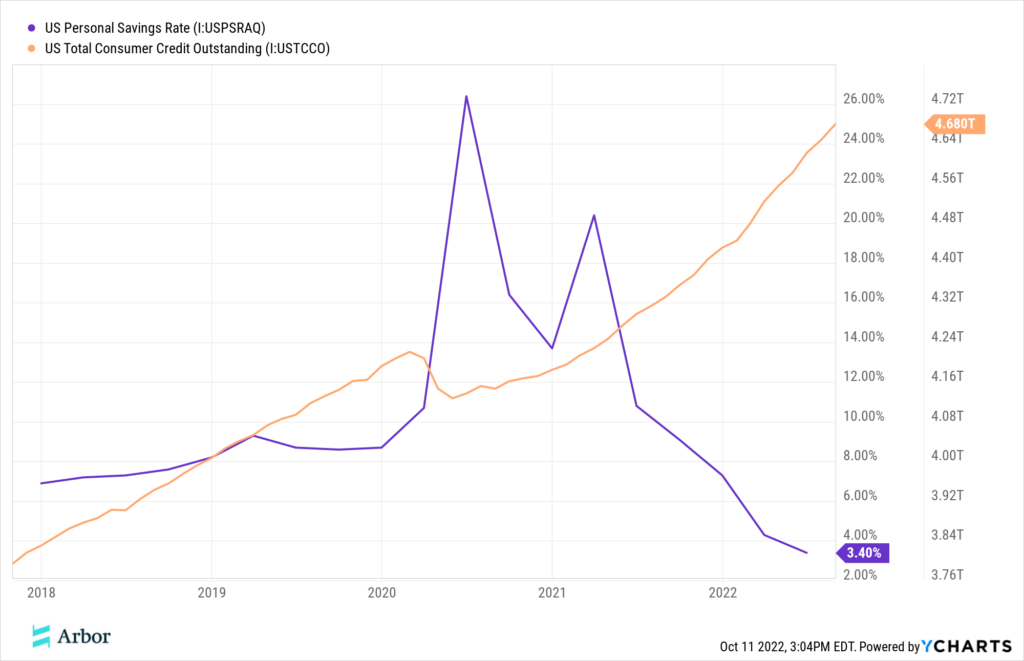

Speaking of inflation, we might be seeing signs of lower inflation coming, oil is down about 40%, used cars are down about 12% and global freight rates are down 67%. Even rents and home prices are falling for the first time since 2011. Unfortunately, inflation has out-paced wage growth for about 18 months. The result is falling US savings rates and increased consumer debt as shown below.

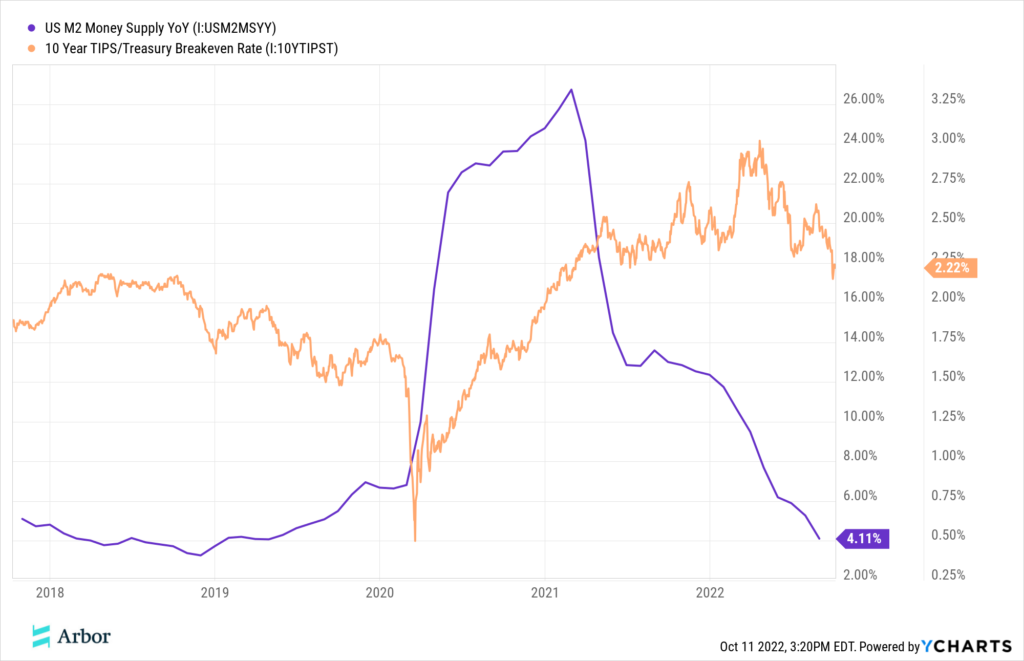

These are not signals of a healthy economy, but they may be signals of slowing inflation. The year-over-year growth rate in the US money supply continues to move down. At 3.4%, it’s below the historical average of 7.2%. Market-based expectations of inflation also continue to fall. The 10-year breakeven inflation rate moved down to 2.22% at the end of September, an 18-month low. These are all positive indicators of slowing inflation.

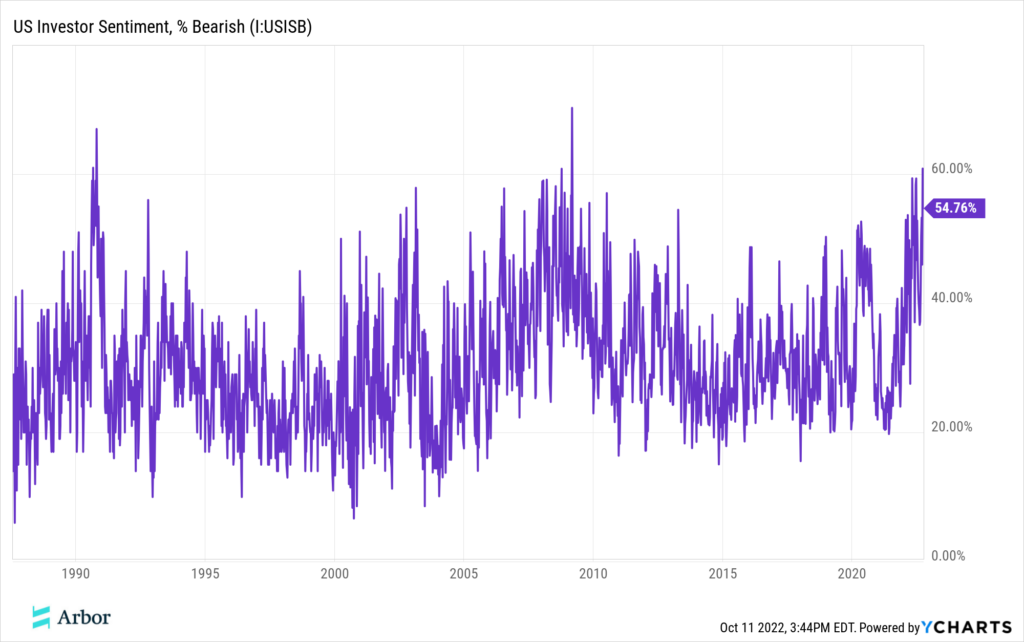

If the market year ended today it would be the first time ever that both the S&P 500 and bond market was down more than 10% for the year. Not surprisingly this has led to extreme negative investor sentiment. The chart below shows that investors are the 3rd most bearish they have ever been since 1990.

The silver lining is that historically, fear is good. Investors have seen above-average forward returns in cases following bearish sentiment extremes. While it’s impossible to time the market “bottom”, it’s reasonable to presume that sticking to your long-term investment strategy is going to be more successful over time than trying to time the market by selling and buying back at the right time. We think there is potential for greater downside as the market shifts from inflation fears to recessionary fears, but if the Feds pivot on interest rates as a result, the market is likely to react positively.

You don’t have to be a master of the stock market to achieve financial independence during the later years of your life. We encourage everyone to create a financial plan that includes a low-cost investment plan. One that is designed to weather these types of economic cycles and market cycles so that you don’t run out of money when asset values fall, while still not missing out on market upside when asset values appreciate. There is plenty of historical precedent to support these strategies, especially when you work with a tax expert to stay tax efficient along the way, while keeping investment costs down.