Retirement income planning is typically more complicated than what first meets the eye. It’s not very difficult to plan gross income. Maybe you plan on taking 5% of your assets a year along with Social Security. Of course, you’ve adjusted this number for inflation and you decide you will probably die around 92, leaving your last check to bounce! Perhaps you have an annuity paying you a guaranteed income stream out of your IRA for life, or a pension with lifetime payout. It’s fairly easy to predict the gross income from these items, and we can project 10 to 20 year annual returns along with inflation, but what about taxes and medical expenses?

Not always so easy. In retirement Social Security is only taxable if you make “too much money”. IRAs are fully taxable to the extent of pretax contributions and growth, but Roth IRA distributions are not when qualified. Annuities are taxable to the extent of gain, passive income from investments and real estate can go either way. Ok.. Ok.. you get the point. Retirement income planning is far more complex than just plugging your gross income numbers into a calculator and running them 20 years out.

One often missed item of consequence are Medicare Part B premiums. The higher your adjusted gross income is, the higher the premiums deducted from your Social Security will be. You are penalized for making to much money!

Is it a good time to go back and discuss why it’s not good to have to much money in an IRA yet? 😊

Medicare Part B premiums

According to the Centers for Medicare & Medicaid Services (CMS), most people with Medicare who receive Social Security benefits will pay the standard monthly Part B premium of $135.50 in 2019. However, if your premiums are deducted from your Social Security benefits, and the increase in your benefit payments for 2019 will not be enough to cover the Medicare Part B increase, then you may pay less than the standard Part B premium.

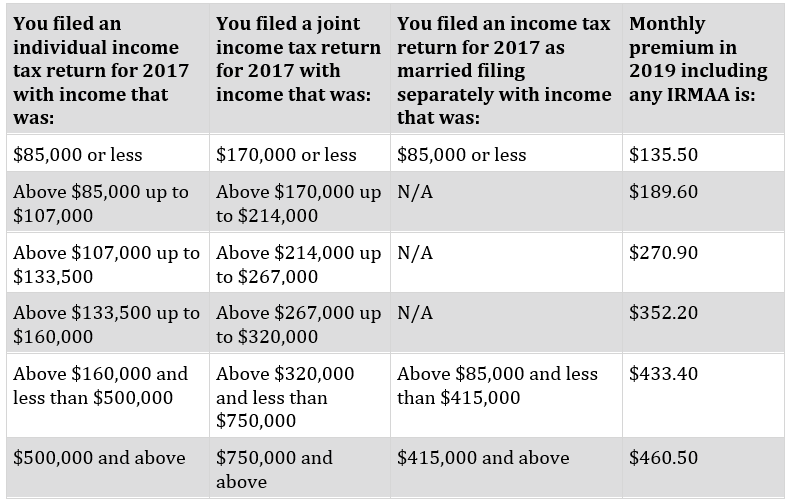

People with higher incomes may pay more than the standard premium. If your modified adjusted gross income as reported on your federal income tax return from two years ago is above a certain amount, you’ll pay the standard premium amount and an Income Related Monthly Adjustment Amount (IRMAA), which is an extra charge added to your premium, as shown in the following table.

Other Medicare costs

Other Medicare Part A and Part B costs in 2019 include the following:

-

The annual Medicare Part B deductible for Original Medicare is $185.

-

The monthly Medicare Part A premium for those who need to buy coverage will cost up to $437. However, most people don’t pay a premium for Medicare Part A.

-

The Medicare Part A deductible for inpatient hospitalization is $1,364 per benefit period. An additional daily coinsurance amount of $341 will apply for days 61 through 90, and $682 for stays beyond 90 days.

-

Beneficiaries in skilled nursing facilities will pay a daily coinsurance amount of $170.50 for days 21 through 100 in a benefit period.

The increase in Medicare Premiums with increased income is often considered immaterial to a retirement plan, but in many cases it is not. Knowing the income limits can help you with questions like, where do I take more of my money? Should I pull the next $20,000 from a taxable source or tax free source? Should I work a little less? Should I do more Roth conversions before I get to retirement?

Make sure you are working with a professional who is asking these questions for you. If you aren’t, call us at 480-818-8300.